For the last several years, discussions around global currencies have often revolved around one big question: Is the dollar losing its grip? The headlines have been dramatic — de-dollarization, reserve currency challenges, geopolitical fragmentation, and a world supposedly moving beyond U.S. financial dominance.

But the data tells a more nuanced story.

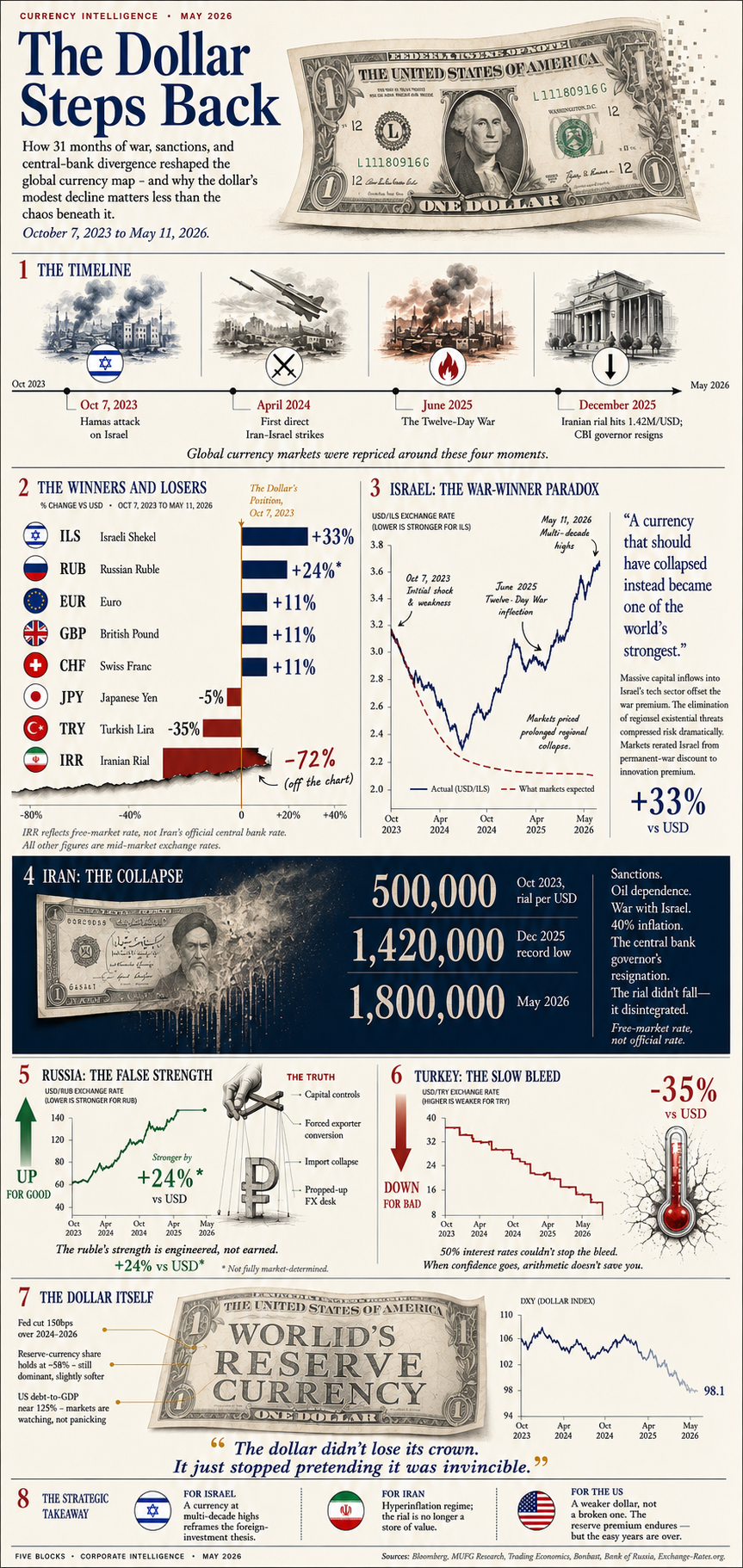

From October 2023 through May 2026, the U.S. dollar broadly weakened. The DXY index drifted from roughly 106 to 98 — a meaningful move, but hardly a collapse. This wasn’t the end of the dollar era. It was a fairly normal cyclical response to Fed easing and changing interest-rate dynamics.

The more interesting story happened beneath the surface.

Currencies around the world began reflecting radically different realities. Israel experienced one of the period’s most surprising outcomes: a currency that many expected to weaken sharply instead became one of the strongest performers globally, as risk perceptions shifted and markets repriced long-term assumptions.

Iran moved in the opposite direction. Its currency didn’t simply decline; it effectively stopped functioning as a reliable store of value. Inflation, sanctions, war, and structural weaknesses combined into something far more severe than ordinary FX weakness.

Russia appeared strong — but with a large asterisk. The ruble’s performance reflected policy intervention, capital controls, and engineered conditions rather than traditional market dynamics.

Turkey continued a story markets know well: extremely high interest rates alone cannot restore confidence once credibility erodes.

What emerges from the period is not a story of dollar collapse. It is a story of divergence.

Some currencies strengthened. Others disintegrated. Some were supported by policy. Others were overwhelmed by geopolitics. The dollar simply stepped back slightly while the rest of the world experienced extraordinary turbulence.

Perhaps that is the real lesson.

The dollar didn’t lose its crown.

It just stopped pretending it was invincible.